When inflation runs hot, a family of four is spending $200–$400 more per month on groceries alone compared to three years ago. That is $2,400–$4,800 a year in silent losses, without buying anything extra. For preppers, inflation is not just an economic inconvenience—it is a slow-motion emergency that erodes your budget, your stockpile purchasing power, and your financial resilience at the same time. Here is how to fight back on every front.

Why Inflation Is a Prepper Problem, Not Just a Financial One

Standard financial advice during inflation focuses on budgeting and investing. That is fine as far as it goes. But preppers face an additional layer: the supplies you need for emergency preparedness—food, water storage, fuel, medical gear—all cost more during inflation. Every month you delay building your stockpile, you pay higher prices for the same pound of rice. Inflation is an argument for buying essential supplies earlier, not later.

The prepper approach to inflation has two tracks running simultaneously:

- Defensive: Stretch every dollar further through strategic shopping, cutting waste, and eliminating non-essential expenses.

- Offensive: Buy forward—build your physical supply stockpile at today’s prices before inflation erodes your purchasing power further.

💡 Tip: Your pantry is an inflation-beating investment

A 50 lb bag of white rice at $0.80/lb today costs $40. If food inflation runs at 6% annually for three years, that same bag costs $47.64. Buying a year’s worth of rice now at $0.80/lb is a 24% three-year return with zero market risk. No stock does that with that kind of certainty. Every can and bag you buy today at current prices is money protected from tomorrow’s prices.

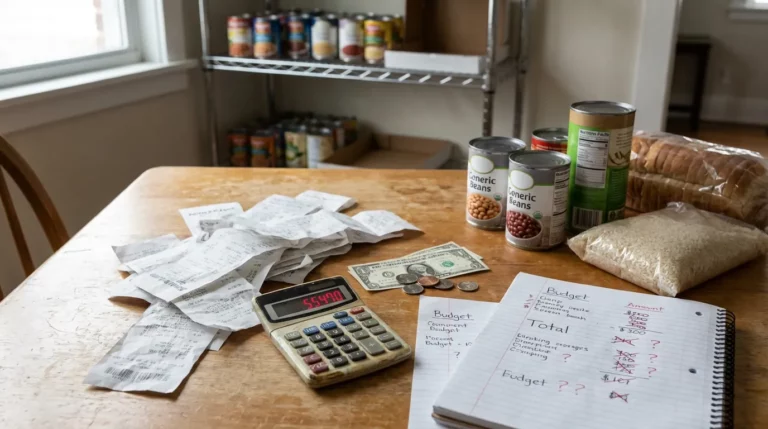

The Prepper Grocery Strategy

Grocery spending is the most immediate place inflation hits a prepper family. The average US family of four spent over $1,000/month on groceries in 2024. Getting that number down 15–25% without sacrificing nutrition requires a system, not just willpower.

Strategic Bulk Buying: What Works and What Does Not

Bulk buying saves money only when you buy things your family actually uses and that store well. Buying 20 lbs of flour that goes stale is not savings—it is waste. The categories where bulk buying reliably wins:

| Category | Best Bulk Source | Shelf Life | Typical Savings vs. Retail |

|---|---|---|---|

| White rice | Costco, Sam’s Club, restaurant supply | 25+ years sealed | 30–40% |

| Dried beans and lentils | Costco, Azure Standard | 10+ years sealed | 25–35% |

| Canned vegetables and fruit | Costco, case lot sales | 3–5 years | 20–30% |

| Pasta and oats | Costco, restaurant supply | 5+ years sealed | 20–30% |

| Cooking oil | Costco, Sam’s Club | 1–2 years unopened | 25% |

| Honey and salt | Costco, restaurant supply | Indefinite | 30–40% |

A Costco membership costs ~$65/year. Most families recover that in the first two bulk purchases. If your household is not already a member, run the math on your annual dry goods spending—it almost always pencils out.

Grocery Apps That Actually Pay

Stack these three tools on every grocery run:

- Flipp app (free): Aggregates weekly sale flyers from every grocery store within your zip code. Find what is on sale before you shop, not while you are in the store.

- Ibotta (free + cash back): Earn $0.25–$1.50 cash back per item on branded goods. On a $200/week grocery run, consistent Ibotta use returns $15–30/week for most families.

- Store loyalty app: Kroger, Safeway, and most major chains give digital coupon access through their apps. Many also offer 10-point fuel rewards per qualifying purchase.

The Prepper Meal Planning System

Meal planning reduces food waste by up to 30% and eliminates impulse buys. For a prepper family, meal planning also serves the dual purpose of rotating your stockpile so nothing expires. The system:

- Plan 7 dinners on Sunday around what is on sale and what needs to be rotated from your pantry

- Build the shopping list from the plan, not the other way around

- Cook in batches on weekends—a double batch of chili or soup saves 45 minutes midweek

- For a family of 4: target a grocery spend under $225/week by replacing one or two meat-centered dinners with bean or egg protein sources ($0.10/serving vs. $1.50+ for beef)

Build Your Pantry as an Inflation Hedge

This is the part most financial advisors skip but every prepper understands: physical food storage is a better inflation hedge than most financial products. You are buying certainty at today’s prices.

✅ Action: The $50/week inflation defense plan

Set aside $50/week from your grocery budget for stockpile building. That is $2,600/year. In 12 months at that rate, a family of four can have:

- 200 lbs of white rice (~$160, enough for 2,000+ servings)

- 100 lbs of dried beans (~$80, 1,000+ servings)

- 50 lbs of oats (~$40, 500+ servings)

- 48 cans of canned vegetables (~$60)

- 24 cans of canned meat: tuna, chicken (~$72)

- 20 lbs of pasta (~$25)

- Honey, salt, sugar, oil (~$100)

- Remaining budget for freeze-dried foods, variety items, and container sealing

This is over a year of core calories for four people, bought at 2026 prices instead of 2028 prices.

Slash Your Monthly Fixed Costs

Fixed expenses are where most families have the most untapped savings. Unlike groceries, which fluctuate weekly, fixed monthly bills can often be cut once and stay cut.

The Subscription Audit

The average American household pays for 4.5 streaming and software subscriptions while actively using 2.1 of them. Audit yours today:

- Pull your bank statement for the last three months

- List every recurring charge over $5

- Cancel anything you have not used in the past 30 days

- For services you keep: can any be shared with another household? (Disney+, Spotify Family plan ~$17/month covers 6 accounts)

Cell Phone: The Biggest Fixed-Cost Win

Most families overpay by $100–$200/month on cell service. The math for a family of four:

| Provider | 4-Line Plan | Network | Annual Cost |

|---|---|---|---|

| Verizon / AT&T | ~$200–$240/month | Tier 1 | ~$2,640 |

| Mint Mobile (4 lines) | ~$60–$80/month | T-Mobile network | ~$840 |

| Visible (Verizon MVNO) | ~$100–$120/month | Verizon network | ~$1,320 |

| US Mobile (4 lines) | ~$60–$100/month | Verizon + T-Mobile | ~$960 |

Switching from a major carrier to Mint Mobile or Visible saves a family of four $1,500–$2,000 per year with virtually identical coverage on the same towers. That is your entire annual stockpile budget right there.

Other Fixed-Cost Cuts

- Insurance: Get competing quotes every 12–18 months. Auto + homeowner insurance prices vary 20–40% between providers for identical coverage. Takes 45 minutes, saves $300–$800/year.

- Internet: Call your ISP once a year and ask for a retention discount. Most will offer 10–20% off rather than lose you as a customer.

- Gym membership: If you have not been in 60 days, cancel it. Use YouTube workouts and a $30 jump rope instead.

Reducing Transportation Costs

For most families, transportation is the second or third largest monthly expense. Gasoline, car payments, insurance, and maintenance compound quickly.

- Gas rewards credit card: The Citi Custom Cash card (~5% cash back on your top spending category) earns maximum returns at the gas station for families who drive a lot. On $300/month in gas, that is $15/month or $180/year in cash back.

- GasBuddy app (free): Finds the cheapest gas within your radius. Price differences of $0.15–$0.30/gallon are common in most metro areas. On a 60-gallon monthly fill for a family vehicle, that saves $9–$18/month.

- Consolidate errands: Plan your week so each car trip covers multiple stops. Reducing 2 solo trips to 1 combined trip cuts fuel use 15–20% with zero lifestyle sacrifice.

- Telecommuting: If your job allows 2–3 days remote per week, you can cut commute costs by 40–60%. That is 40–60% less fuel, 40–60% less wear on your vehicle.

Build an Inflation-Resistant Emergency Fund

40% of Americans cannot cover a $400 unexpected expense. That is the definition of a family that cannot weather inflation without going into debt. Your emergency fund is your buffer between a budget surprise and a credit card balance that grows at 24% APR.

Where to Park It

A regular checking account or savings account earning 0.01% interest loses ground to inflation every single day. Your emergency fund should be in a high-yield savings account (HYSA) that currently offers 4.5–5.5% APY.

- Marcus by Goldman Sachs: Consistently competitive rates, FDIC insured, no fees

- Ally Bank: 4.5%+ APY, no minimum balance, strong mobile app

- SoFi: Up to 4.6% APY with direct deposit set up

For a family of four, the target is 3–6 months of essential living expenses. If your monthly essentials (mortgage/rent, utilities, groceries, insurance) run $3,500/month, your target is $10,500–$21,000 in the HYSA before you move on to other investing.

✅ Action: Automate your way to the emergency fund

Set up an automatic transfer of $200/month to your HYSA the day after your paycheck hits. People who automate savings build funds 20% faster than those who save “what’s left over”—because there is never anything left over without automation. At $200/month at 5% APY, you hit $10,500 in 4 years and change.

Inflation-Hedging Investments for Preppers

Once your emergency fund is funded and your stockpile is building, consider these inflation-resistant financial positions:

| Investment | Inflation Protection | How to Access | Notes |

|---|---|---|---|

| Series I Savings Bonds | Rate adjusts with CPI every 6 months | TreasuryDirect.gov | $10,000/year per person limit; hold 1 year minimum |

| TIPS (Treasury Inflation-Protected) | Principal adjusts with inflation | TreasuryDirect, brokerage | Best in tax-advantaged accounts (IRA) |

| Gold and silver (physical) | Hard asset, 5,000-year track record | APMEX, JM Bullion, local coin shop | Store securely; sells at a premium during crises |

| Real estate (if owned) | Property and rental values rise with inflation | Direct ownership or REITs | Lock in a fixed-rate mortgage now before rates rise again |

| Physical supplies | Guaranteed “return” = avoided future price increase | Costco, bulk food suppliers | Zero market risk; liquid in the only way that matters during a crisis |

⚠️ Warning: Do not neglect debt during high inflation

High-interest debt (credit cards at 20–29% APR) destroys your inflation strategy faster than any other single factor. No investment reliably returns 25%. If you are carrying credit card balances while building a stockpile, pay off the cards first—every dollar of 25% APR debt eliminated is a guaranteed 25% return. Start with the highest-interest balance and work down.

Common Mistakes in Inflation Prepping

1. Buying the wrong bulk items. A 50 lb bag of something your family won’t eat is not savings—it is waste with extra steps. Only buy in bulk what you already consume regularly. Rotate what you store into your meals. First in, first out.

2. Not switching cell carriers. Most families overpay $1,200–$1,800/year on cell service out of inertia. The networks MVNOs (Mint Mobile, Visible, US Mobile) run on are identical to the majors. Switching takes one afternoon and saves more than almost any other single action you can take.

3. Keeping the emergency fund in a regular savings account. At 0.01% interest, a $15,000 emergency fund loses $700+/year in real purchasing power against 5% inflation. Move it to a HYSA today. Takes 20 minutes online.

4. Waiting to buy supplies until after the emergency. Supply chains strain during high inflation events and during disasters. The family that builds their six-month stockpile before they need it pays today’s prices. The family that buys during a shortage pays a 40% premium—if it is available at all.

5. Ignoring fixed costs while obsessing over grocery coupons. Saving $3 on laundry detergent with a coupon while paying $240/month for cell service you could get for $60 is misallocated effort. Cut the big fixed costs first. Coupon second.

6. No budget system at all. You cannot manage what you do not measure. Use a zero-based budget app like YNAB ($14/month or $99/year) where every dollar has a job, or use a free spreadsheet. Either works. Neither is optional if you are serious about surviving high inflation with your finances intact.

FAQ

How much should a family of 4 spend on groceries to stay within a tight inflation budget?

The USDA moderate cost plan for a family of four runs about $1,050/month in 2024. A thrifty household can get that to $650–$750/month with meal planning, store brand substitutions, strategic bulk buying, and minimal food waste. Your baseline target: cut your current grocery spend by 20% before looking for cuts elsewhere. For most families, that is $150–$250/month in immediate savings.

Is it worth buying a Costco membership just for inflation prepping?

For most families of four, yes. The $65/year membership pays for itself on the first two to three bulk grocery runs for staples like rice, pasta, canned goods, and cooking oil. The savings on paper towels, toilet paper, and laundry supplies alone often cover the membership. If your family spends over $200/month on groceries, a Costco membership almost certainly delivers positive ROI.

What is the best way to protect my savings from inflation?

Short answer: high-yield savings account for your emergency fund, I-Bonds for medium-term savings, and diversified index funds with some TIPS exposure for long-term. Do not leave cash sitting in a checking account. Even a 4.5% HYSA partially offsets inflation. The worst thing you can do is nothing—leaving $20,000 in a 0.01% savings account during 5% inflation costs you $1,000/year in real purchasing power.

How do I stretch my food budget without the family noticing the cuts?

Substitute protein sources rather than eliminating them. Dried beans at $0.08/serving vs. ground beef at $1.50/serving—mixed into the same chili or taco recipe, most families do not notice. Switch to store brands on packaged goods: taste tests consistently show 80% of people prefer the store brand when the label is hidden. Add one “pantry meal” per week using only items already on hand. That four-meals-from-the-pantry-per-month habit alone saves most families $80–$120/month.

Should I pay off debt or build my emergency stockpile first during high inflation?

Start with one month of emergency expenses in your HYSA, then attack high-interest debt (anything over 10% APR) aggressively before extending the stockpile. The guaranteed “return” of eliminating 25% APR credit card debt beats almost every investment option available. Once high-interest debt is gone, split surplus cash: 50% to extend the emergency fund, 50% to the stockpile. Once the emergency fund is at three months, the stockpile gets the full surplus.

Inflation is a problem you solve with systems, not willpower. The families who come out of an inflationary period with their finances intact are the ones who cut the right costs early (cell phone, subscriptions, insurance), moved their savings to a HYSA, built their physical stockpile at today’s prices, and paid down high-interest debt before it compounded. None of those moves requires sacrifice—they require a decision and an afternoon to implement. Make the moves now, and your future self pays last year’s prices for everything that matters.

Dan Lockland is a preparedness instructor and survival skills educator with over 15 years of hands-on experience. He shares practical, no-nonsense guidance on emergency preparedness, self-reliance, and sustainable living at PreparingWithDan.com.